C-BLOCK, FLAT NO, RAJAGIRI VALLEY P O, CN-3, Kalangad Rd, Kakkanad, Kerala 682039

Phone Number

9349829440

Email Address

felix@insurancesuperhub.in

Understanding Cashless And Reimbursement Claim Procedures

Dec 02, 2025

by Felix A

Introduction: Why This Matters for Every Policyholder

Having health insurance provides a financial safety net during medical emergencies. But simply owning a policy isn’t enough — it’s equally important to understand how to access your benefits at the time of hospitalization.

What’s the difference between a cashless claim and a reimbursement claim? Both serve the same purpose — helping you recover medical expenses — but the process, timelines, and convenience levels differ. Knowing how each works will help you make informed decisions during treatment.

What is a Cashless Claim?

Definition: In a cashless claim, the insurance company directly settles the hospitalization expenses with the hospital. You don’t need to pay from your own pocket upfront, except for expenses not covered by the policy (like food, toiletries, etc.).

When is it Available?

Only at network hospitals that have an agreement (empanelment) with the insurance provider.

Requires pre-authorization from the insurer, usually at the time of admission.

How Does a Cashless Claim Work?

Choose a network hospital from your insurer’s approved list.

Inform the hospital’s insurance/TPA desk about your health policy.

The hospital sends a pre-authorization request to the insurance company.

The insurer verifies your coverage and gives approval.

After treatment, the insurer directly settles the approved bill with the hospital.

Note: Any non-covered expenses or deductions are paid by you directly to the hospital (if Safeguard+ Add-On is not opted.)

Advantages of Cashless Claims

✅ No need to arrange large sums upfront

✅ Simplifies process during emergencies

✅ Reduces paperwork for the insured

✅ Direct settlement between insurer and hospital

What is a Reimbursement Claim?

Definition: In a reimbursement claim, the policyholder pays all medical expenses at the time of hospitalization. After discharge, they submit the required documents to the insurer, who reimburses the eligible expenses as per policy terms.

When is it Used?

When treatment is taken at a non-network hospital

If cashless approval couldn’t be arranged in time (emergency cases)

When the insured prefers a hospital of their choice, outside the network

How Does a Reimbursement Claim Work?

Pay all hospital expenses yourself.

Collect all original bills, reports, and discharge summaries.

Submit the claim form and documents to your insurer.

Insurer reviews the claim as per policy guidelines.

Reimbursement amount is credited to your bank account.

Typical Timeline: 7-15 working days post submission of complete documents. Some insurers may take 30 days for reimbursement claims.

Advantages of Reimbursement Claims

✅ Freedom to choose any hospital or doctor

✅ Useful in emergencies where network hospitals aren’t accessible

✅ Policy benefits remain intact even without cashless availability

Cashless vs. Reimbursement: Key Differences at a Glance

Aspect

Cashless Claim

Reimbursement Claim

Hospital Type

Network hospitals only

Any hospital

Payment

Insurer pays directly to hospital

Insured pays first, then claims

Documentation

Minimal (handled by hospital/TPA)

Insured collects and submits

Approval Process

Pre-authorization before treatment

Post-treatment document review

Timeline

During hospitalization (quick)

After discharge (7–30 days avg.)

Convenience

High

Moderate

Out-of-pocket expenses

Minimal (non-medical only)

High upfront, reimbursed later

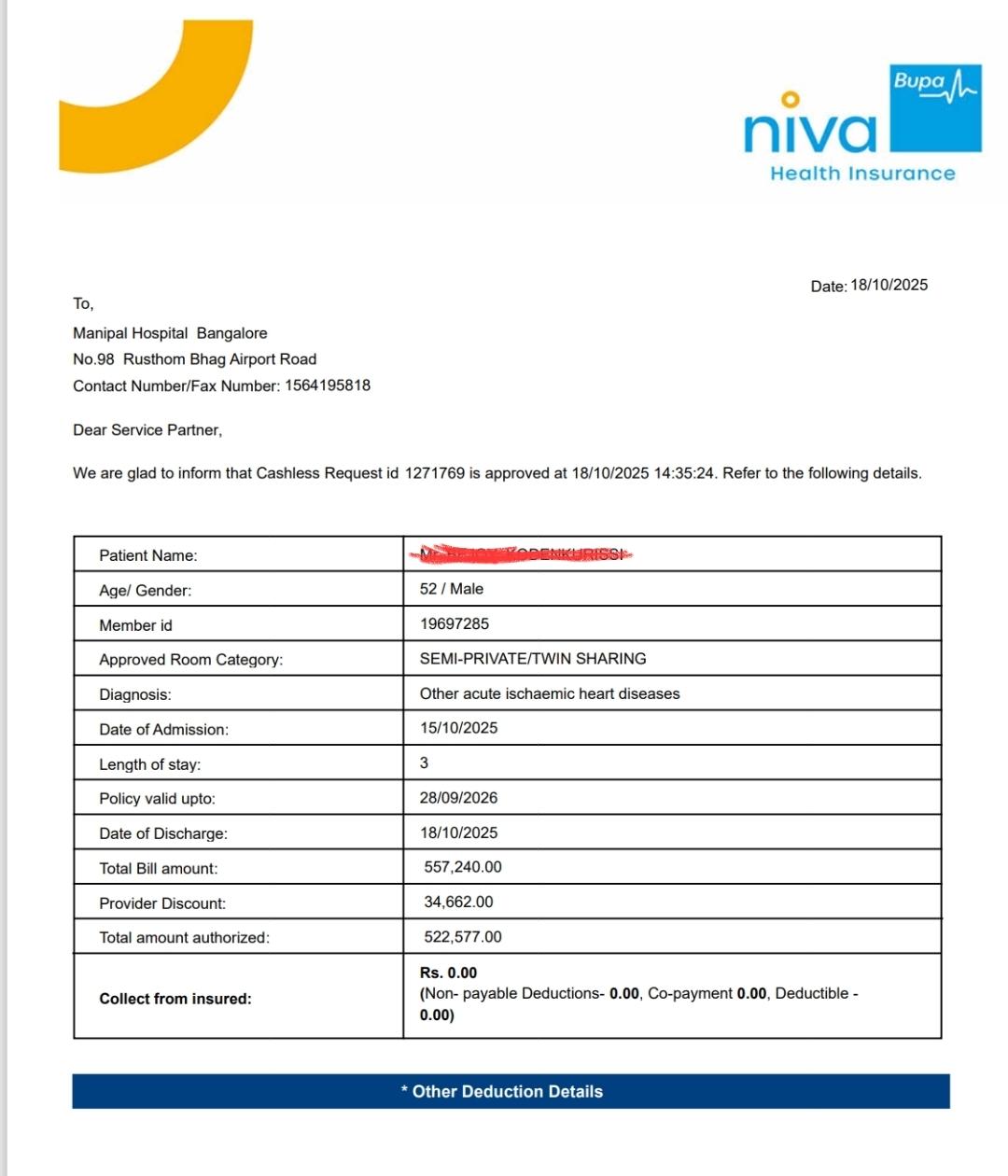

If Safeguard+ Add-On is Opted, then all non-medical/consumable items listed in Annexure list 1-4 will be covered. There won' be any out of pocket expenses. Pls refer the final discharge confirmation received from company👇

When Should You Use Which?

Scenario

Recommended Claim Type

Planned treatment at a network hospital

Cashless

Emergency treatment at a network hospital

Cashless (if possible)

Treatment at a hospital outside the network

Reimbursement

No time for pre-authorization

Reimbursement

Common Misunderstandings About Claims

❌ Myth 1: Cashless means no payments at all. ✅ Reality:Some expenses like consumables, registration, and non-medical items may still need to be paid by the patient.

❌ Myth 2: Reimbursement claims always take months. ✅ Reality:Most insurers process them within 7-30 working days if documents are complete.

❌ Myth 3: Reimbursement is a backup; cashless is always better. ✅ Reality:Both serve valid needs. Reimbursement provides flexibility when cashless is not feasible.

How Advisors Can Help Customers Navigate Both Processes

Explain the difference clearly at the time of policy sale

Share updated network hospital lists

Guide clients on documentation requirements

Set realistic expectations about timelines

Provide support during hospitalization

A well-informed customer experiences fewer hassles and greater satisfaction during claims.

Conclusion: Both Claims Options Serve the Same Goal — Financial Protection

Both cashless and reimbursement claims exist to ensure that you’re financially protected during medical emergencies. The main difference lies in the process and convenience, not the coverage. Understanding these options in advance helps you choose the most suitable path during treatment and reduces stress during already difficult times.

by Felix A

by Felix A